What it measures

Credit spreads compare the yields of high‑yield (junk) corporate bonds with equivalent‑maturity U.S. Treasuries. They indicate the extra compensation investors demand for taking on corporate default risk. A narrow spread suggests strong risk appetite and easy financial conditions, while a wide spread signals stress and heightened default risk.

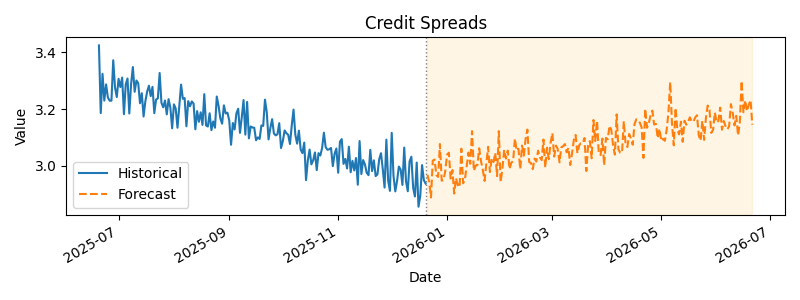

Recent trend

The ICE BofA U.S. High Yield Index option‑adjusted spread hovered near 3 % through late 2025, reflecting historically tight spreads. By mid‑December 2025 the spread was about 2.95 %, close to multi‑year lows. Credit markets remain rich; RBC notes that investors require only about 0.85 percentage‑points of extra yield over Treasuries. This suggests strong risk appetite but leaves little cushion if economic growth slows.

Six‑month outlook

RBC expects corporate issuance and a maturing business cycle to put upward pressure on spreads. With the economy slowing, high‑yield bond supply is likely to increase while investors may demand higher risk premiums. Over the next six months spreads could widen toward the mid‑3 % range, though a severe recession could push them above 4 %. The base case is a modest widening as growth normalizes.

Signal

Current signal: Yellow. Credit spreads remain near multi‑year lows, indicating strong risk appetite. However, with the business cycle maturing and supply of bonds set to rise, spreads may widen, so caution is warranted.